VWAP Momentum Trade¶

- This sample is based on:

from pyalgotrade import strategy

from pyalgotrade.barfeed import yahoofeed

from pyalgotrade import plotter

from pyalgotrade.tools import yahoofinance

from pyalgotrade.technical import vwap

import os

class MyStrategy(strategy.BacktestingStrategy):

def __init__(self, feed, instrument, vwapWindowSize):

strategy.BacktestingStrategy.__init__(self, feed)

self.__instrument = instrument

self.__vwap = vwap.VWAP(feed[instrument], vwapWindowSize)

def getVWAPDS(self):

return self.__vwap

def onBars(self, bars):

vwap = self.__vwap[-1]

if vwap == None:

return

shares = self.getBroker().getShares(self.__instrument)

price = bars[self.__instrument].getClose()

notional = shares * price

if price < vwap * 0.995 and notional > 0:

self.order(self.__instrument, -100)

elif price > vwap * 1.005 and notional < 1000000:

self.order(self.__instrument, 100)

def build_feed(instruments, fromYear, toYear):

feed = yahoofeed.Feed()

for year in range(fromYear, toYear+1):

for symbol in instruments:

fileName = "%s-%d-yahoofinance.csv" % (symbol, year)

if not os.path.exists(fileName):

print "Downloading %s %d" % (symbol, year)

yahoofinance.download_daily_bars(symbol, year, fileName)

feed.addBarsFromCSV(symbol, fileName)

return feed

def main(plot):

instrument = "aapl"

vwapWindowSize = 5

# Download the bars.

feed = build_feed([instrument], 2011, 2012)

myStrategy = MyStrategy(feed, instrument, vwapWindowSize)

if plot:

plt = plotter.StrategyPlotter(myStrategy, True, False, True)

plt.getInstrumentSubplot(instrument).addDataSeries("vwap", myStrategy.getVWAPDS())

myStrategy.run()

print "Result: %.2f" % myStrategy.getResult()

if plot:

plt.plot()

if __name__ == "__main__":

main(True)

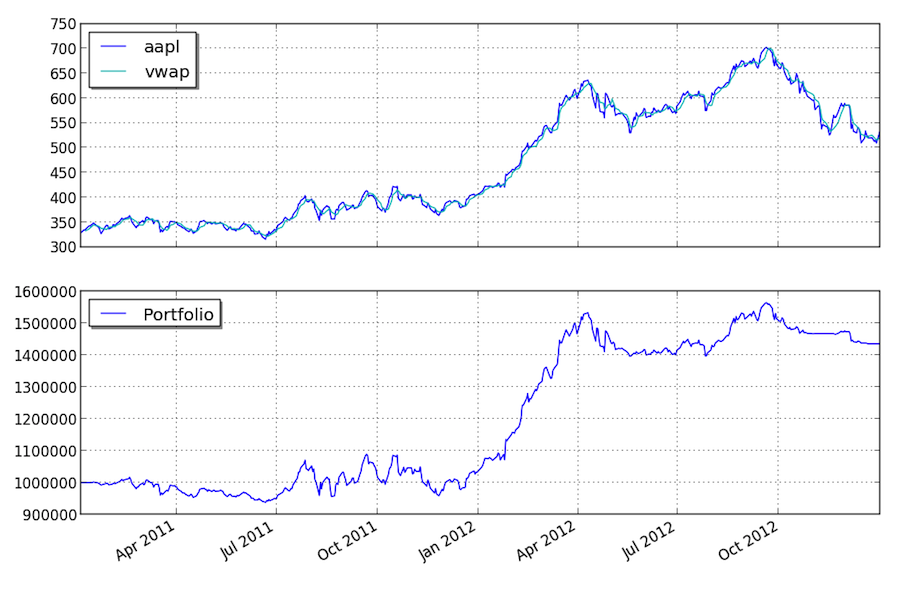

this is what the output should look like:

Downloading aapl 2011

Downloading aapl 2012

Result: 1436098.00

and this is what the plot should look like:

you can get better returns by tunning the VWAP period as well as the entry and exit points.